A fintech go-to-market strategy is a framework for bringing a financial product to market. It covers positioning, distribution channels, customer acquisition, compliance, trust-building, and retention rather than focusing on marketing alone.

People often take longer to evaluate financial products than other types of software. A new task management tool might be tested on the same day it is discovered. A payments platform or investment app can involve account verification, personal information, and financial risk, which naturally changes how decisions are made.

This creates a different set of challenges within the fintech sector. Interest alone does not tell you very much. A product may attract registrations, only for large numbers of users to stop during verification or account setup. Those points often reveal more about adoption than traffic or awareness numbers. Regulatory requirements can also affect onboarding and market entry decisions.

For many financial technology companies, the question is not whether people know the product exists. The question is whether they feel comfortable taking the next step — which is why onboarding, education, community engagement, and ongoing testing tend to receive so much attention during a launch.

Revealing How Fintech Go-To-Market Works

A fintech go-to-market strategy is a commercial framework that aligns positioning, customer acquisition, compliance, onboarding, and retention around a specific financial product.

A budgeting app may attract thousands of registrations, yet a much smaller number of people actually connect their bank accounts. Similar drop-offs can occur with lending platforms, payment products, and investment tools. The difference between initial interest and real usage often becomes visible when customers are asked to verify their identity, provide information, or link financial accounts.

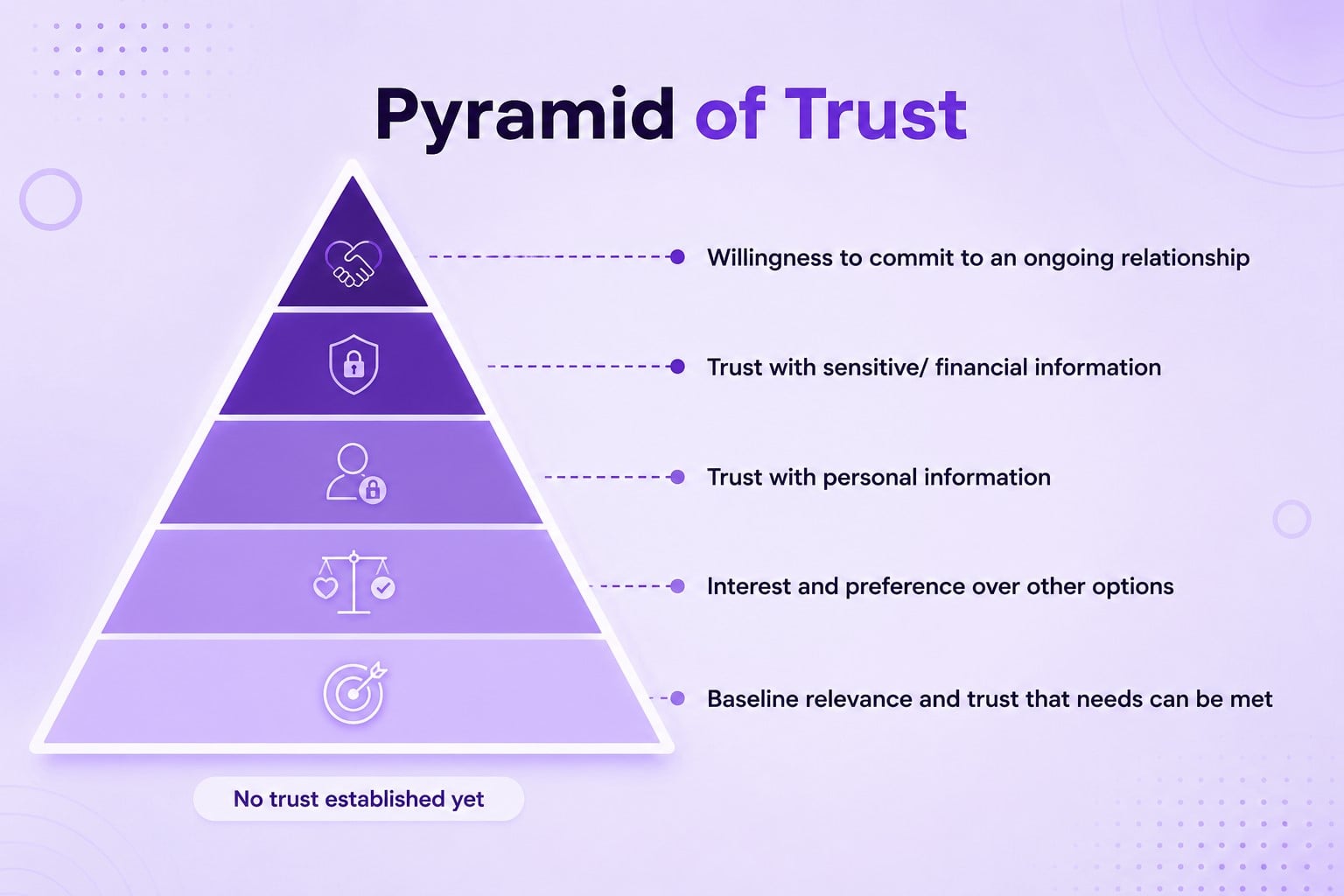

Consumer trust in financial services often becomes relevant before a customer completes onboarding.

Most fintech products ask customers to hand over something valuable:

- Money

- Personal data

- Transactions

- Financial decisions

Before comparing products, some customers look for basic information about the company behind them. Security, regulation, and the handling of customer funds are common areas of interest.

| Traditional SaaS GTM | Fintech GTM | Why It Changes Execution |

| Product-first messaging | Trust-first messaging | Customers evaluate risk before features |

| Fast sign-up journeys | Verification-heavy onboarding | KYC affects conversion rates |

| Marketing-led acquisition | Marketing and compliance alignment | Regulations influence growth channels |

| Conversion focus | Education and conversion focus | Financial decisions require more research |

| Scale quickly | Validate trust before scaling | Poor trust increases churn |

Regulation can shape growth efforts just as much as marketing decisions. What a company can say, how customers are onboarded, and which markets can be targeted may all depend on the rules that apply to the product.

In practice, trust, compliance, education, and retention often become customer adoption barriers when they are overlooked.

“Trust in fintech does not come from perfect design or clever copy. It is built by reducing uncertainty at the moments when users are most likely to hesitate. Clear pricing, transparent explanations of how money and data are handled, relevant customer stories, and visible support options during onboarding all help reassure prospective customers and make it easier to move forward with confidence.”

Vincent N, Lead Strategist at NinjaPromo

Trust is not built entirely inside a product. Many fintech companies also use PR for fintech to establish credibility before customers reach the onboarding stage.

Step-by-Step Framework for a High-Performing Fintech Go-To-Market Strategy

Fintech products can fail at several different points long before growth becomes a concern. Some solve a problem that customers do not consider urgent. Others attract interest but lose users during verification or onboarding. There are also products that gain traction in one market and then run into regulatory issues when expanding. In many cases, these challenges cannot be solved simply by adopting the latest fintech marketing trends. They should be evaluated within the context of customer needs, product-market fit, and regulatory requirements. The sections below look at the areas that tend to have the biggest influence on launch performance.

Align Fintech Offerings With Real Market Demand, Not Product Features

Many fintech companies describe what their product does before establishing why it matters. The strongest fintech products are often tied to a specific operational problem. Delayed payments, high remittance costs, manual compliance work, and restricted access to capital are all examples of issues that can justify a switch to a new provider.

This distinction influences positioning. A company offering real-time payments is not really selling payment infrastructure. It is addressing delayed cash flow. A lending platform is not simply offering financing. It is addressing restricted access to capital. The same pattern appears across the industry. Adoption tends to happen when the underlying problem is obvious and expensive enough to justify change.

| Market Friction | Customer Impact | Fintech Opportunity |

| Slow payments | Delayed cash flow | Real-time payments |

| High transfer costs | Reduced margins | Cross-border payment platforms |

| Compliance workload | Operational inefficiency | RegTech automation |

| Limited lending access | Growth constraints | Alternative credit models |

| Fraud risk | Financial losses | Fraud prevention tools |

Understanding demand is one of the key components of a go-to-market plan for fintech products. Before investing heavily in growth, it is worth answering a few practical questions:

- What financial problem exists?

- How do customers currently solve it?

- What does the problem cost them?

- Is demand growing?

- Is the problem urgent enough to trigger switching?

The responses often point to where demand is strongest and where it is weakest. They can also highlight whether customers see the problem as serious enough to justify changing the way they currently operate.

They may also reveal how crowded the market really is. If ten providers are solving the same problem in roughly the same way, the challenge may not be acquisition but positioning.

This is not unique to fintech. In many B2B go-to-market strategy discussions, the starting point is the problem itself rather than the product being offered.

Apply Regulatory and Compliance Alignment

Problems linked to compliance often surface close to launch. A registration process that seemed straightforward may require additional verification steps, while marketing materials may need to be rewritten to satisfy regulatory requirements.

In practice, compliance influences several parts of a fintech launch:

- KYC requirements — identity verification during onboarding

- AML procedures — transaction monitoring and checks

- Data privacy rules — customer data collection and storage

- Financial disclosures — mandatory risk and product information

- Advertising restrictions — limits on claims and promotions

- Regional licensing — approval requirements by market

Many regulatory compliance requirements directly influence the user experience. A lengthy identity verification process, for example, may satisfy compliance obligations but also increase drop-off rates during onboarding. Decisions made by compliance teams can therefore affect customer acquisition just as much as marketing decisions.

| Situation | Potential Impact |

| Launching in a new country | Additional licensing requirements |

| Running financial ads | Disclosure obligations |

| Updating onboarding | Extra verification steps |

| Expanding product features | New compliance reviews |

Requirements can change from one market to another. A product that can be launched quickly in one country may need additional approvals or onboarding changes elsewhere. These issues are usually easier to address before launch than after launch plans have already been finalised. This often requires a unique approach that accounts for financial trust as well as regulatory obligations.

Use Social Media Marketing as a Trust and Education Channel

A person considering a new budgeting app might spend a few minutes researching it before signing up. Someone considering a lending platform or investment product may spend days or weeks doing the same thing. The financial risk is higher, so the amount of scrutiny tends to increase as well.

This behaviour changes the role social media plays during a launch in the fintech industry. In many cases, potential users are not looking for promotions. They are looking for evidence that the company is legitimate, active, and willing to answer questions publicly.

Content commonly used by fintech brands includes:

- Product walkthroughs

- Industry commentary

- Founder insights

- Customer questions and answers

- Regulatory or market updates

For many products, education becomes part of adoption. Users may understand the problem they are facing but have little experience with the type of solution being offered. That is particularly common in the go-to-market strategy for fintech platforms entering newer or less familiar categories.

This is one reason fintech social media marketing often focuses on visibility and explanation at the same time.

“The biggest mistake is treating market entry as a translation problem. You localise the language, maybe the currency, and assume the rest transfers. It rarely does. What actually changes from market to market is regulation, payment behaviour, baseline trust in financial products, and the signals that make a product feel legitimate or suspicious. Teams that skip local customer research before scaling acquisition often end up optimising campaigns around positioning that was never quite right to begin with. Spend the first 30–60 days validating demand and testing messaging. Only then scale.”

Vincent N, Lead Strategist at NinjaPromo

Leverage SEO to Capture High-Intent Fintech Demand

Not every potential customer discovers a product through advertising or social media. Many begin with a search query. Google reports that 49% of consumers use Search to discover or find new products, making it one of the places where product research often starts.

The intent behind that search often matters more than the search volume itself. Different queries often appear at different stages of the buyer journey in fintech. Someone researching “best expense management software” is usually much closer to evaluating solutions than someone reading a general article about business finance.

In fintech, high-intent searches often fall into four categories:

| Search Type | Example |

| Solution-focused | international payment platform |

| Comparison | X vs Y payment provider |

| Product-specific | business lending alternatives |

| Educational | how to reduce payment processing costs |

A person searching for payment providers, lending options, or compliance tools is usually further along than someone who has only seen an advertisement. This is one reason fintech SEO focuses on connecting products with people who are already looking for answers.

Run PPC Campaigns With a Compliance-First Performance Approach in Fintech

A fintech company can receive plenty of clicks and still learn very little. The numbers may look promising until people reach identity verification, document uploads, or account linking. That is often where the more useful information starts to appear.

PPC can reveal those patterns relatively quickly, making it easier to test audiences, messages, and offers before larger budgets are committed.

| Metric | Why It Matters | What It Reveals |

| CAC | Acquisition efficiency | Cost of growth |

| Cost per qualified lead | Lead quality | Audience relevance |

| Activation rate | Product adoption | Post-click performance |

| KYC completion rate | Onboarding success | Friction levels |

| LTV: CAC ratio | Scalability | Long-term viability |

Consider two campaigns promoting the same product. One might generate a large number of registrations, only for users to abandon the process during identity verification. Another might attract fewer sign-ups but produce a much higher proportion of verified and active users. Looking only at clicks or registrations would miss that difference entirely.

Compliance remains part of the process throughout. Financial products are frequently subject to restrictions around claims, disclosures, and promotional language. As a result, successful campaigns balance experimentation with regulatory requirements rather than treating them as separate considerations.

Many fintech companies use fintech PPC not only to generate visibility but also to gather evidence about which audiences, markets, and offers are most likely to convert into active customers.

Fintech marketing focuses on how companies attract and acquire customers after positioning, onboarding, and compliance considerations have been addressed.

Use Email Marketing to Nurture Trust and Drive Long-Term Fintech Engagement

Not every user who signs up is ready to use a product immediately. Some need more information. Others become distracted during onboarding or stop before completing a key action. Email is often used to bridge that gap.

Common lifecycle campaigns include:

- Welcome onboarding

- Product education

- Activation campaigns

- Re-engagement sequences

- Retention campaigns

Email sequences are often triggered by customer actions rather than fixed schedules.

For many companies, fintech email marketing serves as a way to continue the conversation after registration and encourage regular product usage.

Example of the Real Process Behind Fintech Market Entry

TradeApp entered a competitive market where visibility and audience awareness presented significant challenges.

Several elements of a fintech go-to-market strategy were applied throughout the project:

Identify adoption barriers

Funded trading was not a familiar concept for every prospective user.

Refine positioning

The platform’s offering was presented more clearly through updated messaging and branding.

Increase visibility

The website and brand identity were refreshed to improve recognition.

Educate target users

Educational resources helped explain the platform and the broader trading environment.

Improve engagement

Community interaction created additional opportunities for discussion and feedback.

For TradeApp, the result was a stronger brand presence, improved positioning, expanded educational resources, and a more consistent user experience.

TradeApp’s experience highlights how market entry often involves more than visibility alone. Positioning, onboarding, customer education, and retention are all areas commonly associated with fintech marketing services.

The case also illustrates how a go-to-market strategy for fintech can help improve recognition before growth efforts scale further.

Final Thoughts

Many fintech products can attract interest without attracting long-term users, regardless of how strong the fintech GTM strategy appears on paper. The gap often appears during onboarding, identity verification, or first use rather than during customer acquisition.

A fintech launch framework extends beyond marketing because customers are evaluating more than features alone. They are also deciding whether they trust the company behind the product and feel comfortable using it.

For that reason, adoption is often influenced by factors that have little to do with traffic volumes and much more to do with confidence, understanding, and the overall customer experience. Similar patterns can be seen across products supported by go-to-market agencies.