Key Takeaways

- AI is moving beyond automation as fintech brands use it to guide onboarding and make user journeys more relevant.

- Financial education is becoming a growth tool because it helps users compare offers before sharing sensitive data.

- Niche creators can build credibility when fintech audiences already trust their judgment on financial decisions.

- Privacy and transparency now influence conversion because users want to understand why their data is being requested.

- First-party data helps fintech teams measure lead quality as third-party tracking becomes less reliable.

- Embedded finance brings acquisition closer to the point of need by placing offers inside trusted partner workflows.

Fintech marketing trends show where the old financial growth playbook is starting to break. Customers now compare products faster than brands can explain them, and trust signals often arrive too late. The brands that adapt first are rebuilding how attention turns into confidence.

A fintech company does not lose momentum because it missed one tactic. Growth slows when the product promise no longer matches how customers make financial decisions. That gap shows up in weak onboarding, low-quality leads, and users who hesitate before sharing financial data.

McKinsey’s Global Banking Annual Review describes a move from broad segmentation toward more individualized customer engagement. For fintech teams, that shift makes generic journeys harder to defend.

This guide breaks down the key fintech marketing trends behind that change and shows how financial brands can turn them into stronger customer journeys.

Key Factors Shaping Fintech Marketing and Industry Growth Today

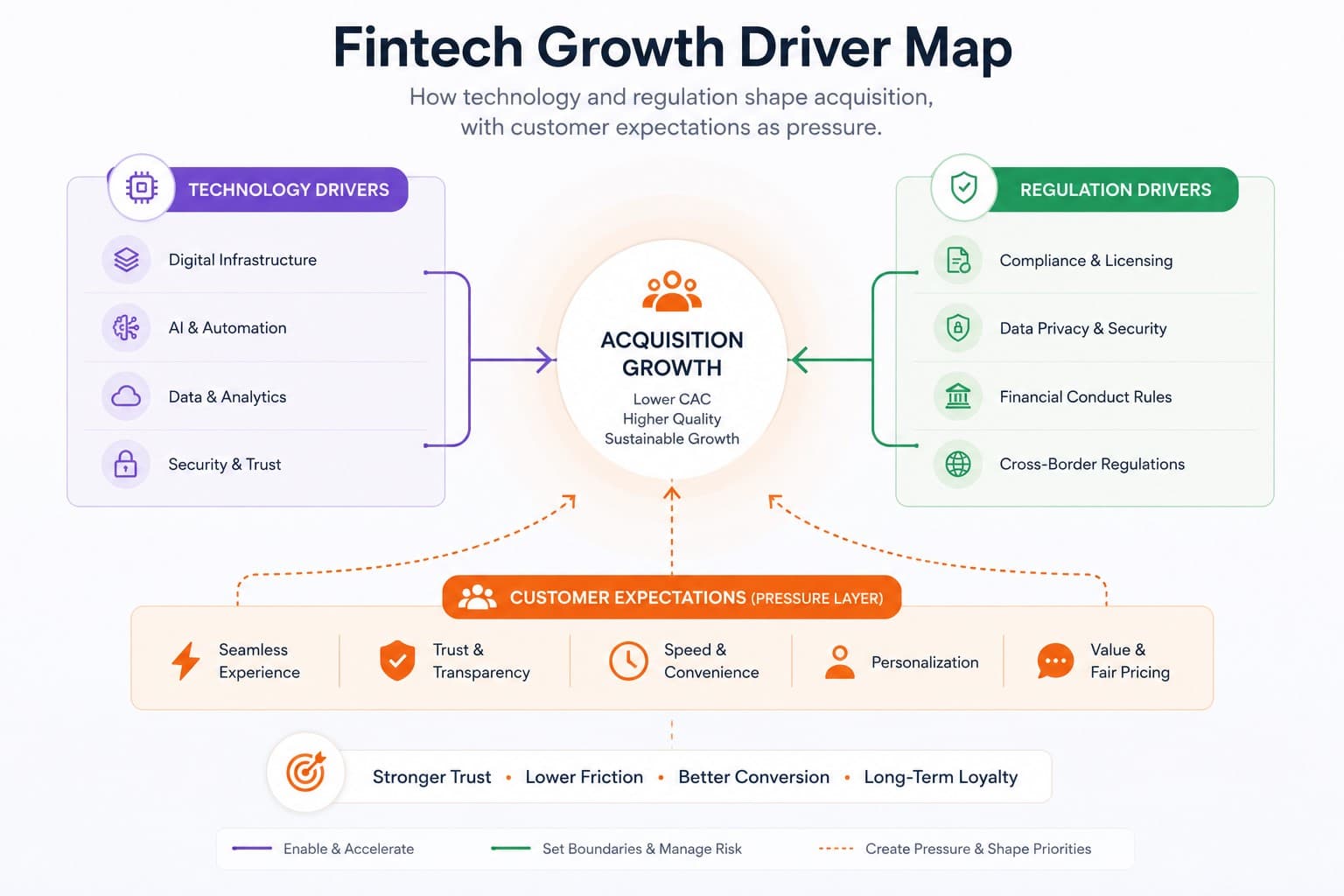

Fintech marketing trends matter when they reflect a real change in customer behavior. The biggest shifts now come from faster product comparison and growing pressure around data collection. These factors shape both acquisition and trust.

AI-driven customer expectations

AI is changing what users expect from fintech products. Now, customers expect personalized experiences based on the information they’ve already shared. If the response feels disconnected, users may question whether the product understood their intent.

For fintech marketers, this sets a higher standard for every step after the first interaction. For example, if a user links an account, the next screen should make the decision easier. If the journey ignores that context, the next step feels less useful.

Stronger regulatory pressure

Regulation shapes how fintech brands describe value. EY’s 2025 regulatory outlook highlights rising scrutiny around disruption, resilience, and financial services risk. That pressure affects marketing before a campaign ever reaches the market.

Growth teams can no longer rely on vague promises or aggressive claims. Before review starts, ads, landing pages, creator scripts, and product explanations need to be clear. A strong campaign should clarify and verify the offer.

Higher trust expectations

Fintech users compare products quickly, but they still move slowly when money or data is involved. Accenture’s banking consumer study identifies trust and personalization as major drivers of customer advocacy. That makes trust part of the conversion path, not just a brand message.

Clear pricing and simple eligibility rules can reduce hesitation. Visible privacy controls help too, especially when a product asks for sensitive data. These signals should appear before the user starts looking for the catch.

First-party data and consent

As third-party signals become less reliable, fintech teams require a stronger foundation of owned data. CRM insights, onboarding behavior, and consent-based signals help marketers identify which leads are likely to activate.

The exchange must feel fair. Users are more willing to share information when they receive clearer guidance or more useful recommendations. Without that benefit, data collection erodes trust.

Embedded distribution

Fintech products are increasingly appearing in partner platforms and everyday workflows. For example, a user may encounter a lending offer in accounting software or a payment option during checkout. This changes the initial marketing moment.

Now, the message must work within someone else’s ecosystem. Timing and context matter more than broad awareness. If the offer seems useful at that moment, embedded finance can shorten the path from need to action.

Together, these factors explain why fintech marketing is moving toward clearer guidance, stronger proof, and more adaptive customer journeys. The brands that respond early can turn trust into a measurable growth advantage.

Emerging Fintech Marketing Trends Financial Brands Should Follow

The most effective marketing strategies are not equally useful for every financial brand. Their value depends on the product model and the decision stage. Trends deserve attention when they help users navigate specific moments with less confusion.

| Trend | Why It Matters | How Fintech Brands Use It |

| Agentic AI | Moves personalization from reactive to proactive | Guides onboarding and next-best actions |

| Financial literacy | Builds trust before conversion | Turns education into qualified demand |

| Niche influencers | Adds human credibility | Reaches communities with specific needs |

| Trust-first marketing | Reduces hesitation | Makes privacy and compliance visible |

| First-party data | Protects targeting quality | Improves segmentation and measurement |

| Embedded finance | Moves acquisition into partner ecosystems | Reaches users at the moment of need |

| Conversational UX | Reduces friction | Supports users with guided answers |

This table is not a checklist to be copied. A wealth app may need educational materials before signup. The same goes for a B2B payments platform, which requires proof of setup time. One useful trend is identifying and solving real barriers in the customer journey.

Agentic AI and Hyper-Personalized Customer Experiences

Agentic AI changes fintech marketing because it can guide the next customer step instead of waiting for another click. McKinsey warns that AI agents could become a key financial interface as customers turn to them for advice. That creates relationship risk for brands that still treat AI as a back-office tool.

Related Articles: Top AI-Driven Marketing Practices for Fintech Success

AI-driven personalization works when it removes uncertainty at the moment a user is about to stop. If someone links a bank account, the next prompt should respond to that signal instead of sending them through a generic journey. If the app ignores that moment, personalization becomes a label rather than a reason to trust the brand.

AI-driven personalization is effective only when it reflects real user behavior, intent, and funnel stage. In crypto, it works best when it helps users understand why the product matters and what action should come next, such as signing up, connecting a wallet, or completing a first transaction.

Maya Miller, Strategist at NinjaPromo

This is one of the fintech innovation trends that should be managed as a product experience. Useful personalization feels timely and understandable. But weak governance makes the same feature feel intrusive.

Financial Literacy as a Core Content and Lead Generation Strategy

Financial literacy works because confused customers rarely convert with confidence. Educational content gives users language for the decision they already need to make. It also attracts people with higher intent than casual campaign traffic.

Interest and readiness to act are not the same thing. Many users read crypto content, follow trends, or engage with educational posts, but qualified leads are the people who have the problem, the intent, and the willingness to take the next step.

Maya Miller, Strategist at NinjaPromo

The best educational content does not sound like a textbook. For example, a credit-building app can explain score movement in plain English. The same goes for a payments platform showing how settlement timing affects cash flow.

This is where intent-based fintech marketing becomes practical. A calculator can qualify demand before a sales touch. Similarly, a guide can prepare the same user before retargeting begins.

Niche Influencer Partnerships

Niche influencer partnerships work because financial decisions need credibility more than celebrity reach. For example, a creator who explains mortgage readiness speaks to people already trying to solve that problem. That relevance gives the campaign a better chance of turning attention into qualified demand.

The mistake is treating finance creators like media inventory. If the audience does not already trust the creator’s judgment, disclosure will not save the campaign from feeling rented. Teams exploring creator-led credibility can use this guide to fintech influencer marketing before choosing a partnership model.

A serious creator will not flatten risk to make the product sound easier. They will ask about pricing and eligibility before endorsing the offer. That friction helps reveal whether the brand story is ready for public scrutiny.

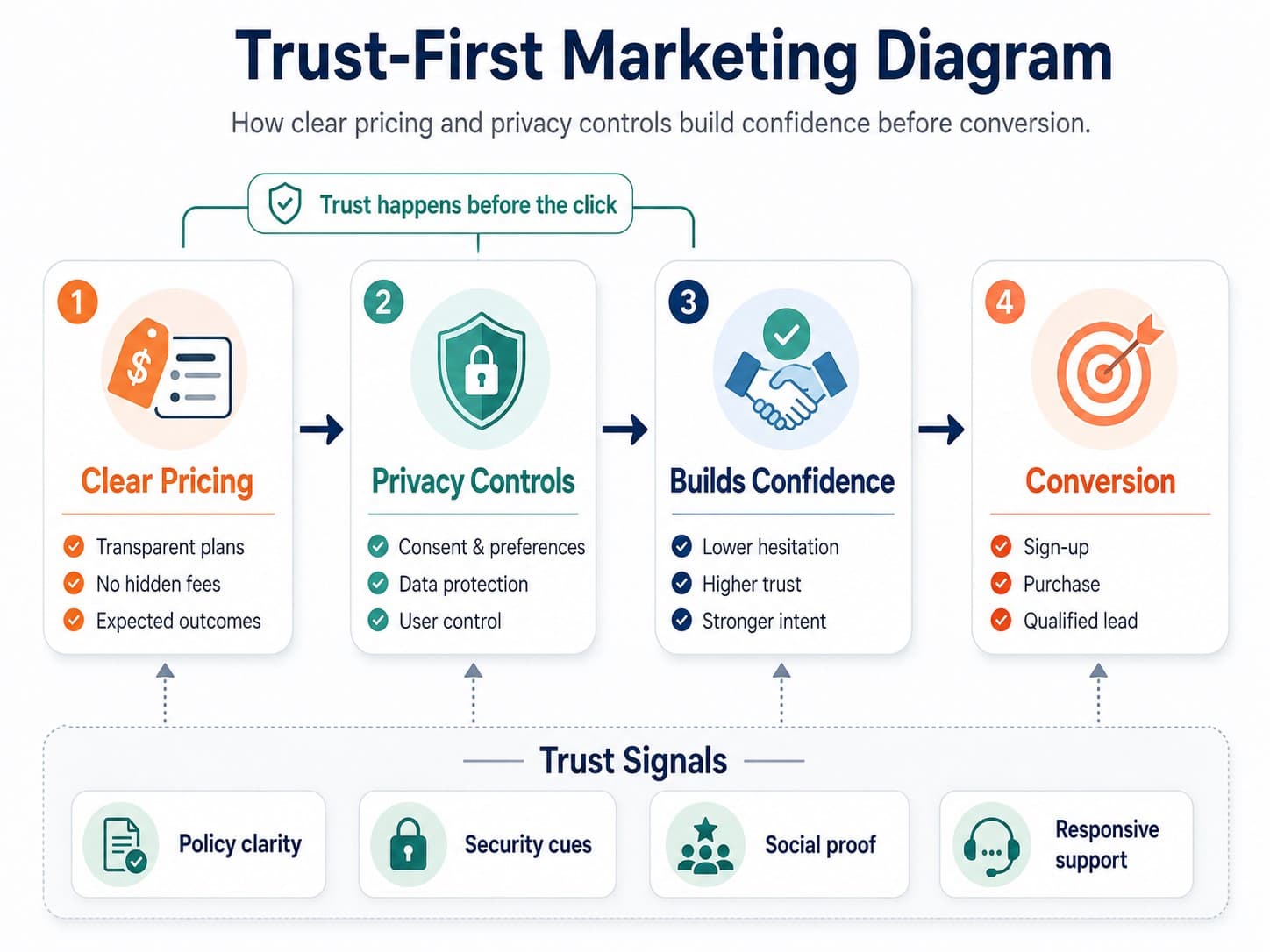

Trust-First Marketing: Transparency, Compliance, and Data Privacy

Trust-first marketing makes proof visible at the moment users judge risk. In finance, trust is more than just a brand idea. It determines whether someone will share sensitive data or move money.

Financial transparency should show up before users start comparing alternatives. Pricing language needs to answer the obvious doubt, while eligibility rules should make the next step feel safe. If customers have to search for hidden conditions, the offer loses clarity.

Regulatory compliance marketing works best when it makes claims easier to verify, not harder to question. Data privacy protection belongs in that same trust layer because financial users notice when a brand asks for more information than the journey requires. A privacy failure weakens consumer trust in financial services long after the technical issue is fixed.

Trust-building in fintech fails when proof arrives after doubt has already formed. A landing page cannot repair a vague ad, nor can a privacy notice save an intrusive form. Clear claims need to appear at the first serious decision point, where the user is deciding whether the brand deserves sensitive data.

First-Party Data Strategies in a Cookieless Future

First-party data matters because fintech teams need customer insight they can defend. When browser tracking weakens, the CRM becomes the place where serious intent either becomes visible or stays guessed. That gives marketers a cleaner way to optimize for activation, not leads that only look efficient inside the ad platform.

The value exchange has to be clear. A user may share financial goals when the product returns a sharper recommendation. If nothing useful comes back, the request feels extractive before personalization has a chance to work.

The biggest trust gap usually appears between interest and the first real action. That action may be creating an account, starting onboarding, connecting a wallet, or signing a first transaction because this is when users begin trusting the product with access, data, or money.

Maya Miller, Strategist at NinjaPromo

The IAB State of Data 2025 report describes the shift toward first-party data and clean rooms as the deprecation of signals reshapes media campaigns. For fintech marketers, designing for consent is now as important as having ad platform skills. Poor data collection creates risk before the campaign even begins.

First-party data also changes how teams judge channel quality. For example, a paid campaign may appear efficient until CRM data reveals weak activation. Better owned data allows marketers to optimize toward account value instead of surface-level leads.

Embedded Finance and Ecosystem-Led Marketing

Embedded finance changes fintech market evolution because acquisition now happens inside someone else’s workflow. A business owner may discover financing when accounting software surfaces a cash-flow gap. That makes timing part of the marketing message, not just a distribution detail.

Deloitte’s embedded banking research shows where the first marketing moment shifts. Users meet the offer inside a platform they already trust. If the value is unclear there, distribution creates reach without demand.

That shift affects the message before the campaign reaches the user. Teams must craft partner narratives before customers see the offer. Ecosystem-led growth fails when the embedded message feels like an interruption rather than a useful next step.

Embedded distribution also changes attribution. The first meaningful interaction may happen inside a partner workflow rather than on the brand’s website. So, marketing teams need shared reporting rules before they can judge whether the partnership is working.

Conversational UX: AI Assistants and Financial Co-Pilots

Conversational UX matters because financial users often need answers at the exact decision point. Static pages can explain features. But they can’t always guide users through repayment choices or account setup.

The strongest use cases reduce friction before it becomes abandonment. For example, a co-pilot can explain a declined transaction. Additionally, it guides customers through product steps that would otherwise trigger support.

Marketing innovation in fintech will increasingly depend on assisted journeys. The brand experience will extend beyond ads and landing pages. It will also include the quality of the responses customers receive when they need help.

How to Evaluate Whether a Fintech Marketing Trend Is Worth Following

Not every marketing trend deserves a budget just because it sounds current. Financial brands should judge each shift by customer need and business impact. The right choice should connect a market shift with a measurable business goal.

| Evaluation Factor | What to Ask | Red Flag |

| Customer need | Does this remove real friction? | It only feels innovative internally |

| Business objective | Which metric should improve? | No link to acquisition or retention |

| Regulation | Can the claim be defended? | Review starts after launch |

| Implementation cost | What resources are required? | Tool cost ignores team capacity |

| Measurement | Can impact be tracked cleanly? | Success depends on vague awareness |

| Scale potential | Can this work beyond a pilot? | It needs constant manual effort |

A trend worth testing should undergo a small but rigorous pilot program. Its purpose is to define the audience and decision point before launch. If the team cannot identify the behavior they want to change, the experiment is not ready.

Financial brands should also separate novelty from advantage. Having an AI assistant does not make a brand more useful. Similarly, a creator partnership is useful only when it improves trust or product quality.

Teams should compare new experiments against wider buyer behavior before making long-term plans. Current B2B marketing trends can help financial brands separate channel noise from durable market shifts. That comparison matters when the same buying committee expects both innovation and risk control.

Implementation cost needs more attention than teams usually give it. A trend may look cheap when the invoice only covers a tool or creator fee. The real cost appears when legal review, data cleanup, or product support starts consuming internal capacity.

Measurement should also begin before the pilot. A good test defines the user behavior that should change rather than just the channel metric that should improve. This approach prevents marketing innovation from becoming just another dashboard with no business decision behind it.

Use this 5-step filter before investing:

- Identify the customer decision causing friction.

- Match the trend to that decision.

- Check compliance and data requirements.

- Run a limited pilot with clear metrics.

- Scale only after proving behavior change.

Final Thoughts

The most useful fintech marketing trends do not focus on chasing novelty. Growth improves when customers receive clearer guidance and stronger privacy signals. A practical strategy begins with the friction customers already experience.

Both AI and first-party data point in the same direction. Customers want financial brands to reduce complexity without hiding risk. This is why trust should be prioritized alongside acquisition.

The future of fintech marketing belongs to teams that test new ideas against real customer needs. Successful teams will test ideas against customer needs before scaling them. This approach transforms innovation into growth rather than noise.