Key Findings

- Trust and security are the foundation of long-term fintech customer retention.

- Frictionless onboarding increases activation and reduces early user drop-off.

- Behavioral personalization strengthens engagement across the customer lifecycle.

- Financial education helps users gain confidence and adopt more fintech services.

- AI-powered insights enable fintech companies to predict churn and improve retention.

Customer retention in fintech focuses on keeping existing users engaged after they join a financial product. Strong retention improves profitability because loyal customers adopt more services and generate greater lifetime value. Companies that understand customer behavior can reduce churn before it affects long-term growth.

Acquiring new users remains expensive across financial services. Retaining existing customers often delivers stronger returns with lower marketing costs. Successful fintech brands therefore invest in trust, education, personalization, and continuous product improvements rather than acquisition alone.

The Biggest Challenges Fintech Companies Face With Customer Retention

Every fintech company loses users for different reasons. Most problems, however, originate from declining trust, confusing experiences, or weak customer engagement. Understanding these barriers creates the foundation for effective customer retention in fintech.

Low Customer Trust in Financial Services

Trust determines whether users keep their money inside a financial platform. Even minor security concerns can encourage customers to move funds elsewhere. Financial decisions involve higher perceived risk than most digital purchases.

Fintech companies must demonstrate transparency throughout every interaction. Clear pricing reduces uncertainty. Visible security practices also reassure customers before problems appear.

Regulatory compliance strengthens credibility. Independent security certifications provide additional confidence. Consistent communication reinforces trust after every product update.

Trust signals fintech customers expect:

- Clear fees before account activation.

- Visible data protection explanations.

- Plain-language security notifications.

- Fast support during sensitive actions.

- Transparent complaint resolution steps.

- Regular updates about product changes.

Poor User Experience and Product Friction

Customers expect financial products to save time, not create extra work. Slow onboarding often causes early abandonment. Confusing navigation also reduces long-term engagement.

Many fintech platforms overwhelm new users with unnecessary steps. Long verification forms create frustration. Unclear product features delay the first successful action.

Common onboarding friction points:

- Too many verification steps.

- Unclear document requirements.

- Slow approval status updates.

- Weak mobile form usability.

- Missing progress indicators.

- Confusing first-action prompts.

Companies should identify friction through behavioral analytics. Session recordings reveal navigation problems. Funnel analysis highlights where customers leave the product.

Small improvements often deliver meaningful retention gains. Faster verification increases activation rates. Simpler interfaces encourage regular product usage.

Lack of Personalization

Generic communication rarely supports long-term loyalty. Customers expect services that reflect their financial goals. Personalization helps brands remain relevant after onboarding.

Behavioral data reveals changing customer needs. Spending patterns identify useful recommendations. Product usage highlights future opportunities.

Behavioral signals for personalization:

- Frequent use of specific features.

- Repeated searches inside the app.

- Changes in transaction frequency.

- Abandoned setup or upgrade steps.

- Support questions about one product.

- Inactive periods after regular usage.

Personalization extends beyond marketing messages. Intelligent dashboards simplify financial decisions. Relevant notifications encourage continued engagement.

Successful fintech customer retention depends on timely recommendations. Every interaction should provide practical value. Irrelevant messaging gradually reduces customer interest.

Limited Customer Engagement After Signup

Many fintech products communicate actively before registration. Engagement often declines after account creation. Customers then forget the product’s long-term value.

Retention requires regular interactions across multiple touchpoints. Educational content answers common questions. Product updates encourage feature discovery.

Post-signup engagement touchpoints:

- Welcome emails after activation.

- In-app tips for unused features.

- Product update announcements.

- Educational alerts during market changes.

- Community invitations for active users.

- Re-engagement messages after inactivity.

Customer communities also strengthen engagement. Peer discussions create confidence. Shared experiences reinforce long-term relationships.

Brands should monitor engagement continuously instead of periodically. Declining activity often predicts future churn. Early intervention improves retention before users leave.

Key Steps for Creating a Successful Fintech Customer Retention Strategy

A successful retention strategy follows a structured process rather than isolated initiatives. Every step should strengthen customer value and reduce unnecessary friction. Consistent execution produces sustainable customer retention in fintech.

| Retention Step | Why It Matters | Primary KPI |

| Analyze customer behavior | Identifies churn risks early | Churn rate |

| Improve onboarding | Accelerates time to value | Activation rate |

| Build a community | Increases engagement | Active users |

| Strengthen social communication | Maintains regular contact | Engagement rate |

| Publish educational content | Builds trust | Feature adoption |

| Personalize communication | Delivers relevant experiences | Open rate |

| Share customer success | Reinforces credibility | Customer confidence |

| Reward loyal customers | Encourages repeat usage | Retention rate |

| Use AI and analytics | Predicts churn proactively | Customer lifetime value |

Analyze Customer Behavior and Churn Drivers

Retention begins with understanding why customers leave. Behavioral data often reveals problems before support teams notice them. Early detection reduces preventable churn.

Monitor activity across the entire customer journey. Look for abandoned onboarding. Track declining feature usage.

McKinsey notes that analytics-driven customer feedback helps banks identify customer needs and trends at scale. Customer feedback adds valuable context. Support tickets expose recurring frustrations.

Combine quantitative and qualitative insights before making product decisions. Individual metrics rarely explain customer behavior completely. Context produces stronger retention improvements.

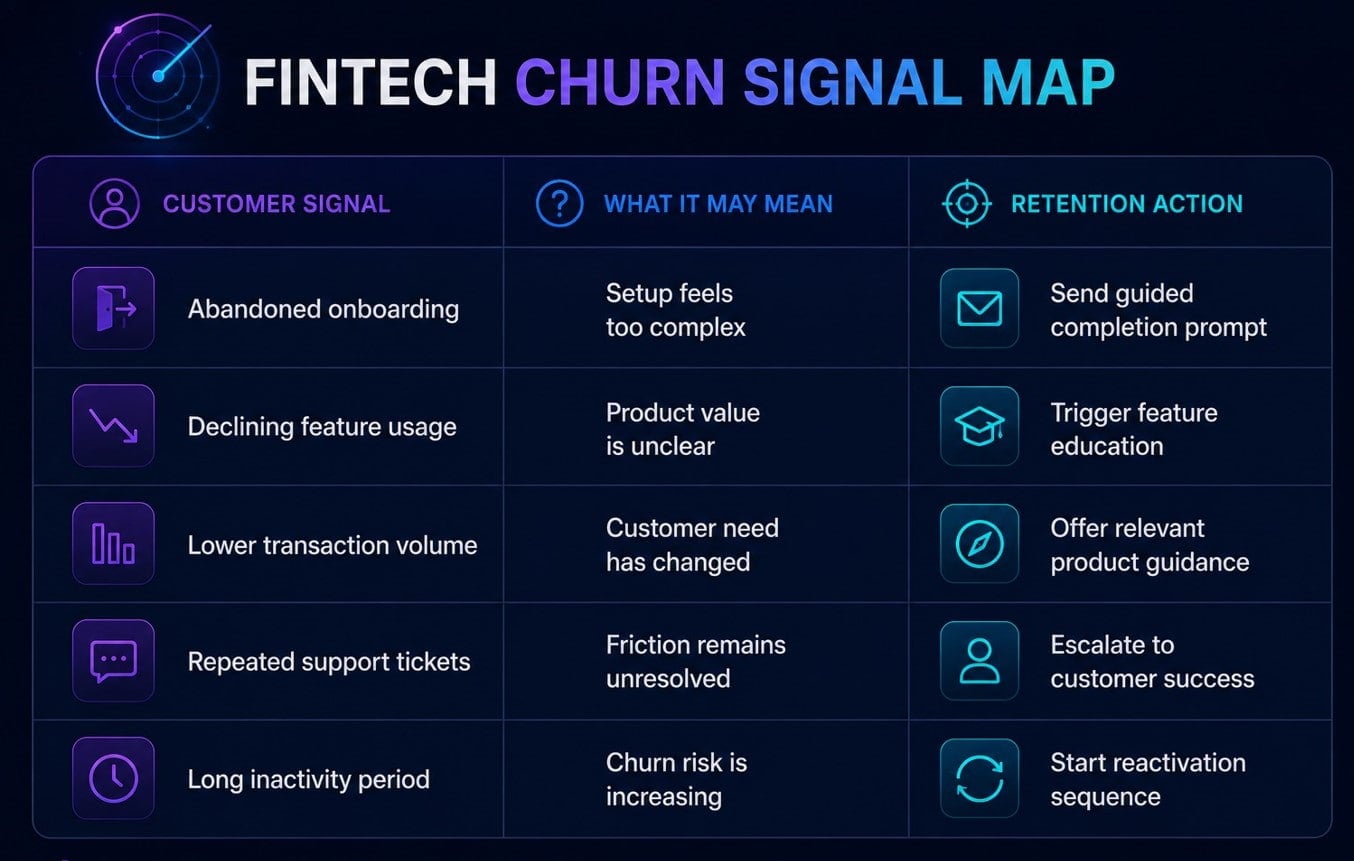

Common churn signals include:

- Declining login frequency

- Inactive premium features

- Unfinished onboarding

- Repeated support requests

- Falling transaction volume

Behavioral segments should reflect real product usage. New users need activation support. Active users need feature discovery. At-risk users need timely reactivation.

Health scores make this process easier. They combine logins, transactions, complaints, and feature usage. Teams can then prioritize users with rising churn risk.

This approach helps teams reduce fintech churn before cancellation happens. It also protects high-value customer relationships.

Improve Onboarding and Product Experience

First impressions strongly influence long-term loyalty. Customers should understand product value within their first session. Delays increase abandonment.

Every onboarding step should serve a clear purpose. Remove unnecessary forms. Explain each required action.

Interactive walkthroughs improve confidence. Progress indicators reduce uncertainty. Contextual guidance simplifies complex features.

Onboarding elements that improve early value:

- Short product tour after registration.

- Clear setup checklist.

- Plain-language verification guidance.

- Contextual tips for first actions.

- Instant confirmation after each step.

- Easy access to support.

Product optimization never stops after launch. Customer expectations continue changing. Regular usability testing uncovers new improvement opportunities. Improving onboarding also strengthens broader fintech marketing efforts because activated users engage more consistently after the first product interaction.

Strong onboarding should define clear activation milestones. A wallet app may track the first deposit. A lending platform may track completed eligibility checks.

Each milestone should move users closer to product value. Progress indicators reduce uncertainty. Contextual tips explain complex financial actions.

This approach improves fintech app retention because users understand value earlier. It also reduces support pressure after signup.

Activation milestones to track:

- Account verification completed.

- First deposit or transfer made.

- First core feature used.

- First security setting enabled.

- First personalized recommendation viewed.

- First recurring action completed.

Create a Community Around Your Product

Communities create stronger customer relationships than one-way communication. Members exchange practical advice. Shared experiences increase confidence.

Successful communities encourage participation instead of promotion. Expert discussions answer complex questions. User feedback shapes future product improvements.

Exclusive webinars strengthen engagement. Customer roundtables generate valuable insights. Educational events reinforce product expertise.

Community formats for fintech retention:

- Expert Q&A sessions.

- Product feedback groups.

- Customer education webinars.

- Private user communities.

- Founder or advisor discussions.

- Peer support channels.

Community participation also supports fintech customer retention. Active members often remain loyal longer. They frequently recommend trusted products to others. Community programs also support fintech inbound marketing by creating useful conversations that attract, educate, and retain customers over time.

Community formats should match the product audience. Consumer fintech brands often benefit from education-led groups. B2B fintech platforms need expert discussions and customer roundtables.

Community managers should track participation quality. Repeated questions reveal product confusion. Active discussions reveal unmet customer needs.

Community signals worth tracking:

- Repeat questions about one feature.

- Growth in peer-to-peer answers.

- Requests for new product guidance.

- Webinar attendance from active users.

- Feedback themes from loyal customers.

- Support topics moving into community discussions.

These insights support a stronger retention strategy for fintech teams. They also help product teams prioritize improvements.

Strengthen Customer Relationships Through Social Media

Social media should support existing customers, not only attract new ones. Regular communication keeps the product visible. Helpful conversations strengthen long-term relationships.

Financial education performs better than constant promotion. Market updates answer timely questions. Product announcements explain new capabilities.

Customer support also belongs on social platforms. Fast responses reduce frustration. Public conversations demonstrate transparency to potential users. A structured fintech social media marketing strategy helps brands maintain regular contact with users between major product interactions.

Social media actions that support retention:

- Reply to product questions quickly.

- Explain updates in plain language.

- Share timely financial education.

- Highlight customer support resources.

- Monitor recurring complaints publicly.

- Invite engaged users into communities.

Build Trust Through Educational Fintech Content

Education reduces uncertainty before customers make financial decisions. Confident users remain active longer. Trusted information strengthens long-term relationships.

Content should solve practical financial problems. Step-by-step guides simplify complex topics. Market analysis explains changing industry conditions.

Educational resources should remain accessible after onboarding. Searchable knowledge bases reduce support requests. Regular newsletters reinforce product expertise. Educational resources should become part of a broader fintech content marketing strategy that continues delivering value after onboarding.

Educational content that supports retention:

- Product tutorials for new users.

- Security guides for sensitive actions.

- Market updates during volatility.

- Feature explainers after product launches.

- Knowledge base articles for common issues.

- Newsletters with practical financial tips.

Educational content should match customer maturity. New users need simple product tutorials. Experienced users need deeper financial guidance.

Market updates can explain risk without creating fear. Product guides can reduce confusion during feature adoption. Security explainers can strengthen customer confidence.

This approach supports financial services retention because trust grows through repeated clarity. Useful content keeps customers engaged between transactions.

Use Personalized Email and In-App Communication

Personalized communication keeps customers engaged throughout their lifecycle. Generic campaigns quickly lose attention. Relevant messages encourage continued product usage.

Behavioral triggers improve communication timing. Spending activity reveals customer interests. Product usage identifies the next logical recommendation.

Personalization should remain helpful rather than intrusive. Notifications should solve customer problems. Every message should support a meaningful action.

High-impact personalization triggers:

- First successful transaction.

- Unfinished account verification.

- Inactive account for several days.

- New feature matching customer behavior.

- Significant change in spending patterns.

- Reached loyalty program milestone.

Lifecycle automation works best when messages follow behavior. An unfinished setup needs a reminder. A new feature needs a short explanation.

Inactive customers may need a simpler return path. High-value customers may need premium support. Frequent users may appreciate usage summaries.

These messages create personalized financial experiences without overwhelming customers. Good timing improves customer retention and reduces communication fatigue.

Best practices for lifecycle communication:

- Limit message frequency.

- Match content to customer goals.

- Use consistent messaging across channels.

- Test different delivery times.

- Measure engagement after each campaign.

- Update workflows using customer feedback.

Effective customer retention depends on delivering relevant communication at the right moment. Better timing increases engagement. Better relevance reduces customer fatigue.

People trust customer experiences more than marketing claims. Authentic success stories demonstrate measurable outcomes. They also reduce uncertainty before customers explore new features.

Case studies should explain real business or personal challenges. The customer journey adds credibility. Quantifiable results strengthen the overall story.

Strong customer stories should include:

- A clear customer challenge.

- The product feature used.

- A measurable outcome.

- A short customer quote.

- A specific use case.

- Proof that feels verifiable.

Testimonials work best when they address specific concerns. Verified reviews increase confidence. Independent ratings provide additional reassurance.

Social proof also benefits existing customers. Positive experiences reinforce purchase decisions. Strong communities naturally create additional recommendations.

Build Loyalty With Rewards and Exclusive Benefits

Loyalty programs give customers a reason to keep using the product. Rewards work best when they support real financial behavior. Empty discounts rarely create lasting loyalty.

Effective rewards may include:

- Premium features

- Lower transaction fees

- Referral bonuses

- Personalized offers

- Early access to new tools

Exclusive benefits should match customer value. Active users deserve stronger incentives than inactive accounts. This approach protects margin while increasing loyalty.

A strong fintech retention strategy connects rewards with meaningful product usage. Customers should feel recognized for valuable actions. That makes loyalty programs easier to sustain.

Leverage AI and Data Analytics to Boost Fintech Customer Retention

AI helps fintech companies identify churn risk before customers leave. According to IBM Institute for Business Value, organizations increasingly use AI to improve customer engagement. Predictive models can detect declining engagement, failed actions, or reduced transaction activity. These signals help teams act earlier.

Analytics also supports better segmentation. High-value users need different communication than new accounts. Inactive customers often need simpler reactivation journeys.

Useful AI applications include:

- Churn prediction

- Personalized offers

- Next-best-action recommendations

- Support automation

- Behavioral risk scoring

Companies investing in AI digital marketing for fintech can combine predictive analytics with automated customer engagement. This approach improves personalization while helping retention teams respond before churn increases.

AI should support decisions, not replace strategy. Retention teams still need clear rules. They must define which signals require action.

For example, reduced activity may trigger education. Failed verification may trigger support. Lower transaction volume may trigger a product recommendation.

These workflows help retain fintech customers with greater precision. They also improve fintech user engagement across the lifecycle.

How Often Should a Fintech Business Review Its Customer Retention Strategy?

A retention strategy requires continuous improvement. Customer expectations change regularly. Product updates also influence user behavior.

Most fintech companies review retention metrics every month. Bain’s work on customer loyalty economics shows why retention rate, customer lifetime, and customer value should be reviewed together. Quarterly reviews evaluate broader strategic changes. Annual reviews help validate long-term business priorities.

Different metrics require different review schedules.

| Metric | Recommended Review Frequency | Purpose |

| Churn rate | Weekly | Detect early retention issues |

| Product activation | Weekly | Measure onboarding success |

| Customer engagement | Monthly | Track product usage |

| Customer satisfaction | Monthly | Identify experience gaps |

| Customer lifetime value | Quarterly | Measure long-term profitability |

| Retention rate | Quarterly | Evaluate strategy effectiveness |

Reviews should always lead to action. Teams should prioritize one improvement at a time. Small improvements compound over time.

Questions worth asking during every review include:

- Where do customers leave the product?

- Which features remain underused?

- Which customer segments show higher churn?

- Which campaigns increase repeat engagement?

- Which onboarding steps create friction?

Customer feedback deserves equal attention. Quantitative metrics reveal trends. Interviews explain why those trends exist.

Continuous improvement supports retention in fintech more effectively than occasional redesigns. Regular adjustments reduce risk. They also strengthen customer relationships.

Final Thoughts

Long-term growth depends on keeping existing customers engaged. Trust, personalization, education, and continuous optimization all contribute to stronger retention. Companies that review performance regularly respond faster to changing customer expectations.

The strongest retention in fintech strategies evolve alongside customer behavior. Small improvements delivered consistently often outperform major product redesigns. Sustainable retention always begins with understanding why customers stay.